Hospitality CapEx Math 101 – Useful Life

Highest and Best Use – CapEx – Part II

CapEx Math 101 – Useful Life

There are four important concepts that hotel owners and operators need to know about CapEx useful life. Applying these concepts is crucial to good CapEx decisions and achieving highest and best use of owner’s capital.

The four important concepts of CapEx useful life:

- Maximize Useful Life

- Match the Investment Horizon

- Consider Risk, Obsolescence, Technology, and Taxes

- Do the Math

Useful Life

Many hotel capital assets just do their job year after year, with minimal inputs of operating expense. Examples of these assets include roofs, exterior walls and windows, water distribution systems, and fire and life safety systems. These assets are great examples of the most basic rule of CapEx useful life:

Maximum Actual Useful Life = Maximum Return on CapEx $

The longer the actual useful life of a capital asset, the lower the costs become per unit of use. In simple terms, a $900,000 roof that must be replaced after 15 years costs about twice as much per year than if the roof’s life is extended to 30 years.

Although it is easier to think about reducing CapEx costs “per year”, extending useful life is beneficial only in delaying the capital expense required to replace the asset. There is really no “per year” benefit; only a delay in expenditure of the total replacement cost.

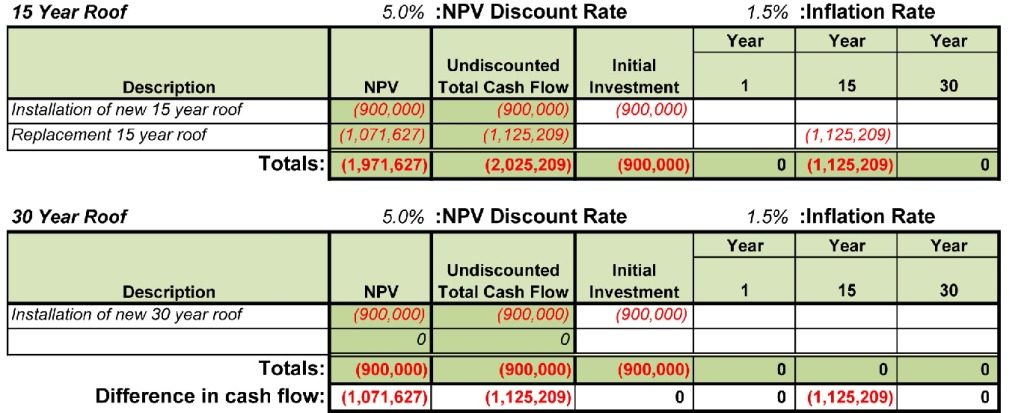

Here is a simple cash flow analysis:

This analysis is oversimplified to illustrate the point, but clearly demonstrates that there is an advantage to maximizing the useful life of this roof. The 15 year roof costs $1,972K ÷ 30 yrs. = $66K/yr. The 30 year roof costs $1,072K ÷ 30 yrs. = $36K/yr.

Maximizing Useful Life

How do you maximize the useful life of capital assets? The concepts are pretty simple, and can be applied to most capital assets.

- Buy the right capital asset to begin with, and

- Take good care of it.

Here are some ideas for the roof example:

Design, Specification, and Installation – For both the initial investment, and any subsequent replacements, it is the owner’s responsibility to ensure that the roof is properly designed, specified, and installed. This is the opportunity to make good decisions about expected useful life, warranties, maintenance requirements, price, and value.

Inspection, Maintenance, and Repair – Roof warranties generally require documentation of inspections, maintenance, and repair before the warranty will be honored. Although it is the operator’s responsibility to ensure that the roof is properly inspected, maintained, and repaired, it is in the owner’s best interest to confirm that this work is being done, and that systems are in place to track and document the work.

The obvious intent of the warranty’s inspection, maintenance, and repair requirements is to extend the useful life of the roof at least until the end of the warranty term. These same measures will continue to help extend the life of the roof beyond the warranty term. It is absolutely possible to extend the actual useful life of a roof 5 to 15 years beyond the warranty period with regular inspection, maintenance, and repair.

There is also the “maintenance paradox” to consider. Well maintained assets are less likely to require repair, and are less costly to maintain over the life of the asset. Poorly maintained assets require more repair work, are more expensive to maintain, typically have a shorter useful life, and are more likely to fail catastrophically.

Finally, it is important to note that extending useful life only applies to existing capital assets, and is almost entirely under the control of the hotel’s operator.

Buy right, and insist that capital assets are well maintained.

Operating Expenses

Capital assets often require ongoing labor, energy, water, maintenance, and repair expenses. In some cases, these annual operating expenses approach or exceed the cost of the capital asset itself.

Capital asset operating expenses typically increase over time. As assets age, they often operate less efficiently and require more maintenance and repair. While operating expenses complicate the analysis of maximized useful life, they do not alter the basic math. For major capital assets, it is important that owners quantify these operating costs, and balance them against the capital replacement costs. Well-functioning capital assets should only be retired when the operating expense balance tips in favor of replacement.

Extend Useful Life until replacement life cycle costs are below current operating costs.

Investment Horizon

Would you replace the $900K roof in the earlier example if you were planning to sell the property in two years? Probably not.

Say the roof had failed, and there was no choice about replacing it. Most owners would choose the least expensive replacement they could find, with the only requirement that it last at least until after the expected sale date of the property. Let the new owner worry about the roof!

Conversely, if this hotel was a “core asset”, and you intended to hold the property for the next twenty or thirty years, you would be well advised to purchase a premium quality new roof with the lowest total life cycle costs.

Coordinating capital asset useful life with the owner’s investment horizon requires good judgement about how these decisions will be factored into the sales price.

- Will the prospective buyer discount the purchase price by the full cost of replacing the worn out roof?

- Should you replace the 30 year old chillers two years before sale, and get the value of the increased operating cash flow from energy and maintenance savings?

- Will the full revenue benefit of a guestroom renovation be reflected in the sale price?

- Will a deferred renovation be discounted in the purchase price by the buyer?

Balance CapEx useful life with owner’s investment plans.

Risk

Operating risk is an important consideration in useful life decisions. Fire suppression, life safety, and security system replacement decisions all carry a substantial element of risk. Failure of one of these systems in an emergency can potentially put a hotel out of business, but replacement is expensive, and has no positive affect on revenue.

Some capital assets also carry regulatory risk. For example, although smoke detectors may continue to function for 15 or 20 years, they have a regulatory useful life of only ten years. They “must” be replaced after ten years by regulation. The regulatory risk penalty is a fine or injunction. The safety risk is a guest or employee death or injury in the event of a fire.

Certain mechanical and electrical systems are critical to the operation of the hotel, and their failure can have a profound effect on the business. For example, a full service Marriott hotel in Virginia suffered the failure of all three of its heating and domestic hot water boilers at the same time. Unfortunately, the failure occurred during the winter, and during a period of high group occupancy.

Had the boilers been replaced in a planned fashion, they would have cost the owner only $275K.

Because of the failure, the owner paid a premium for the replacement boilers, expediting fees, overtime expense for installation, fees for temporary boilers, and substantial rebates to groups using the hotel. The hotel’s reputation was also damaged in a very competitive market, reducing future revenues.

The additional one-time costs associated with the failure were roughly twice the cost of a planned boiler replacement.

Consider operating and regulatory risk.

Obsolescence

While extending the life of some capital assets indefinitely would be ideal (e.g. a hotel’s roof), maximizing the useful life of obsolete assets may require replacing them before the end of their functional life.

For example, 30+ year old chillers in perfect operating condition are not at all unusual in well-maintained hotels, but these machines may be as much as 25% less energy efficient than current technology. Energy savings alone can often justify early replacement of this equipment.

Replace obsolete equipment.

Technology

New technology can eclipse the useful life of a capital asset.

In the early ‘80’s, hotels still had electro-mechanical telephone systems that required an operator to place long distance telephone calls. The charges for the long distance call were printed out by the phone company on a dedicated “HOBIC” teletype machine located in the hotel’s front office, and then manually posted to the guest folio (an actual printed piece of heavy paper or cardstock) using another electro-mechanical machine.

Regulatory changes, and advances in computer technology completely replaced all of this equipment, required no direct labor expense, and improved accuracy and timeliness of transactions. Computerized telephone systems, call accounting systems, and integrated hotel property management systems reduced operating expense and increased revenues. Front office staffing requirements were halved. System “maintenance” was handled remotely at substantially less expense.

New technology completely changed the operation of the telephone department and front office of the hotel, and also required significant new capital asset investments. Of course, all of the old telephone equipment was still perfectly functional, and could have continued to operate for years had its useful life not been eclipsed by new technology.

New technology has driven similar changes in customer relationship management, property management, lighting, lock systems, energy management, accounting, and maintenance management.

Embrace new technology.

Depreciation and Taxes

There are three depreciation and tax questions related to useful life.

One: What happens if you replace a capital asset before it is fully depreciated?

- EBITDA is not affected.

- Owner’s capital is required to purchase the replacement capital asset.

- The owner’s P&L must reflect for both the undepreciated costs of the retired asset, as well as the first year’s depreciation of the replacement asset.

- Owner’s profit goes down by the excess depreciation expense.

- The owner avoids income tax on the decreased profit.

Two: What happens if you replace a capital asset when useful life equals depreciation life?

- EBITDA is not affected.

- Owner’s capital is required to purchase the replacement capital asset.

- Depending on the exact details of the replacement timing, there may be two depreciation payments in a single tax year (one for the old asset, one for the new), or one for the old asset one year, and one for the new asset the following year.

- Profit goes up or down by the change in depreciation expenses.

- The owner pays more or less income tax on the change in profit.

Three: What happens if you extend the useful life of a fully depreciated capital asset?

- EBITDA is not affected.

- Cash is not required to fund purchase of the replacement capital asset.

- Since there is no longer a depreciation expense for the asset on the owner’s P&L, profit goes up by the amount of the avoided depreciation expense.

- The owner pays income tax on the increased profit.

Note that in all three cases, cash flow from operations does not change, owner’s capital cash requirements change in timing but not amount, and depreciation expense changes in timing but not amount.

Any resultant changes in taxable profit will change the timing of taxes paid, as well as the amount of taxes paid due to changes in tax rates or bracket.

Changes in useful life affect the timing of depreciation, taxes, and capital investment, but generally not the amount.

Doing the Math

See how you do on this quick math test:

Which would you pick (actual prices on Amazon)?

☐ Palmolive Dishwashing Liquid, Original (1.32 Gallon) @ $20.49

☐ Palmolive Dishwashing Liquid, Original – 32.5 fluid ounce (Twin Pack) @ $5.66

My mother-in-law can do this math in her head faster than I can pull up a calculator on my phone. Although I can estimate the unit costs for each container in my head, it takes a calculator to bring the answer to 4 decimal places of precision.

- The big container costs ……………………………………. $0.1227 per ounce

- The Twin Pack costs ………………………………………… $0.0871 per ounce

Even though there is a 40% per ounce price difference between the big jug and the twin pack, it doesn’t really matter which container of soap you buy; it isn’t a material expense. However, while overspending on a bottle of soap is no big deal, choosing the wrong capital asset, or paying more than you need for CapEx may affect the financial success of the hotel. The larger the CapEx, the more material the effect on the owner’s financial success.

Once you start considering useful life, inflation rates, revenue effects, energy costs, labor expense, tax effects, and so forth in your CapEx analysis, the math quickly becomes too complex for even my mother-in-law’s capable brain.

- Simplify and state your assumptions and alternatives

- Quantify and include all cash flows

- Itemize other decision factors; risk, obsolescence, etc.

Incorporating these factors in a flexible analysis spreadsheet will allow you to test your assumptions about useful life, operating costs, and timing, and to directly compare the costs of alternative CapEx investment strategies. An example analysis is attached.

Do the Math, test your assumptions.

Summary

Understanding how useful life affects CapEx costs and decisions will help owners achieve highest and best use of their capital dollars.

-

Extend useful life

-

Maintain & repair

-

Keep an eye on operating expense

-

Consider risk

-

Retire obsolete assets

-

Embrace new technology

-

Don’t worry about taxes & depreciation

-

Do the math and test your assumptions

About the Author:

Thomas Riegelman is principal at R-A Associates, LLC and a former member of Cayuga Hospitality Consultants.

Contact Us

Share

Related Articles & Case Studies

News

Joseph Cozza Appointed Partner at Cayuga Hospitality Consultants

SARASOTA, FLA. MAY 20, 2023 Cayuga Hospitality Consultants is excited to announce that Joseph Cozza, based in Farmingdale, NJ, has joined the team...

News

Operations

ChatGPT Accelerates the Evolution of SSI/DID for Personalized Travel Experiences

An article published by Phocuswright suggested that the evolution DID/SSI, Decentralized Identifiers and Self Sovereign Identity, would transform a fragmented travel experiences market...

Operations

Sales, Marketing & Revenue Management

Case Study: B2B Marketing for Management Company

The Challenge: Sharing a TrevPAR Success Story This mid-sized hotel operating company had outperformed other similar businesses during the pandemic in total...